Featured

Table of Contents

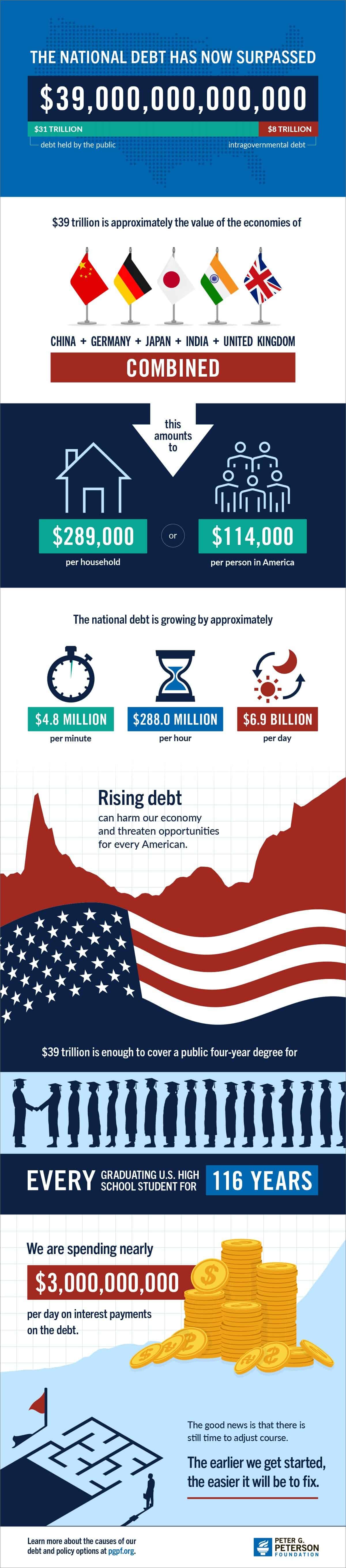

Home debt in America is over 18 trillion dollars, according to the Federal Reserve Bank of St Louis. With so much debt, it's not surprising that numerous Americans wish to be debt-free. If you are searching for financial obligation relief and you wish to state bye-bye to your debt for excellent, take actions to complimentary yourself from your financial institutions in 2026.

Financial obligation is always a financial problem. However it has actually ended up being harder for lots of individuals to handle in current years, thanks to increasing interest rates. Rates have actually risen in the post-COVID age in reaction to unpleasant economic conditions, including a surge in inflation caused by supply chain interruptions and COVID-19 stimulus costs.

While that benchmark rate doesn't straight control interest rates on debt, it affects them by raising or lowering the expense at which banks obtain from each other. Added expenses are usually handed down to customers in the form of higher interest rates on financial obligation. According to the Federal Reserve Board, for instance, the average rate of interest on credit cards is 21.16% as of Might 2025.

Card rate of interest may also increase or stay high into 2026 even if the Federal Reserve changes the benchmark rate, due to the fact that of growing creditor concerns about rising defaults. When financial institutions hesitate consumers won't pay, they frequently raise rates. Experian also reports average interest rates on auto loans struck 11.7% for used automobiles and 6.73% for new cars in March 2025.

Should You File for Relief in 2026?

Personal loan rates are also greater. With many type of financial obligation becoming more pricey, lots of people desire to handle their financial obligation for goodespecially given the continuous financial uncertainty around tariffs, and with a recession hazard looming that could impact employment prospects. If you are scared of rates rising or the economy faltering, positioning yourself to become debt-free ASAP is one of the smartest things you can do.

Even if you aren't worried about rising rates, the longer you bring debt, the costlier it is, the more aggravating it can be, and the harder it is to achieve other goals. Beginning a brand-new year owing money can take a mental toll.

Start by gathering a few essential documents and pieces of information. That can assist you understand what you owe and just how much you can genuinely afford to pay toward ending up being debt-free. Here are the essential steps: Make a complete list of your arrearages, the rate of interest, and the balances due.

Recording Financial Challenge for the IRS in 2026Choosing Reliable Debt Settlement Options in 2026

is a terrific resource for acquiring your credit apply for free, and seeing arrearage at a glimpse. Track your spending. Look at your bank and charge card declarations to track your costs. Utilizing a budgeting app may be valuable here to see exactly how much of your money is going to basics like groceries and bills, and how much is going to non-essentials like eating in restaurants or movie tickets.

Research alters to legal guidelines: For instance, in 2025 through 2028, auto loan interest will be tax-deductible for qualified people as an outcome of provisions in the One Big Beautiful Bill Act. Using the information you gather, identify the following: Total exceptional debtBalance of each debt, and the interest rate you are being chargedWhether interest for each is tax-deductible (keeping in mind that the rules can change with time, so checking once again in future is wise)Due date for regular monthly paymentsFunds you might use towards financial obligation reward Getting arranged offers you a clear image of where you stand, what time frame for financial obligation reward is practical, and what financial obligation relief alternatives deserve pursuing.

The two main methods are the financial obligation snowball and the financial obligation avalanche. Involves lining up your debts from smallest to biggest, and dealing with the tiniest debt. You continue this way with all your debts until you have actually paid whatever off.

Say you have $200 of discretionary earnings in a month, and $10,000 of credit card financial obligation across 5 credit cards. Pay the minimum payments on all five charge card, but designate as much of that $200 as you can to paying off the credit card financial obligation with the smallest balance.

Key Tips for Choosing Pre-Bankruptcy Counseling in 2026

A huge advantage of the debt snowball method is that you settle your very first financial obligation quickly, which might assist motivate you to remain on track. Andr Small, a licensed monetary organizer based in Houston, Texas and creator of A Little Investment, states a number of his low-income customers choose the snowball technique, while people with more discretionary income may be inclined to utilize the debt avalanche.

As with the snowball, make at least the minimum payment for all of your cards, with extra cash going to the card with the greatest APR (annual percentage rate). That very first debt you pay off might not have the tiniest balanceit might even have the highestbut this method saves you money in interest over time vs.

That's because you pay off the costliest debt.

MethodCostTime to FinishCredit ImpactHow it WorksBest ForDebt management planTypically under $50/month3 -5 yearsYesA not-for-profit credit therapy agency negotiates a payment prepare for all of your unsecured debtFull financial obligation payment with professional finance guidanceDebt ConsolidationVariesVariesYesYou take a new loan to pay back numerous existing debts. Lowering your rate (if you qualify for less expensive funding)Balance Transfer3-5%VariesYesYou transfer existing charge card debt onto a new card with 0% balance transfer offer.

A lot of unsecured financial obligations are qualified to be forgiven Chapter 13 involves a 3- to five-year payment strategy. Debtors who require legal defense from creditorsEach choice has advantages and disadvantages. Here's a bit more information about how each works: Financial obligation consolidation: If you qualify for a debt consolidation loan, this can be a terrific alternative.

Evaluating Credit Management Against Bankruptcy for 2026

This simplifies things, given that you have just a single payment. Depending on whether you make your loan term longer or much shorter, it might also reduce overall borrowing costs, as long as you aren't spending for much longer than you were on the loans you combined. Debt settlement: You or a financial obligation relief company work out with financial institutions and get them to accept a swelling sum payment or payment plan for less than the total you owe.

Credit therapy: You work with a licensed therapist to review your finances and determine just how much you can pay towards financial obligation. Credit counselors offer monetary counseling when you enlist in a financial obligation management strategy. That's a structured payment program in which you make one month-to-month swelling sum payment, and that money is distributed to creditors by the debt management business based on terms they have actually worked out.

{kind=link}

Latest Posts

Protecting Your Rights Against Collector Harassment in 2026

Qualifying for Government Financial Assistance in 2026

Choosing Between Settlement and Bankruptcy in 2026